Understanding difference between Medicare parts A, B, C and D can feel overwhelming at first, especially when you hear terms like Part A, Part B, Part C, and Part D. Many people approaching retirement struggle to understand what each part covers, how much it costs, and whether they need additional coverage.

The good news is that Medicare becomes much easier once you understand the basics. To learn more about medicare and supplement, you can also read Medicare Advantage vs Medicare Supplement.

In this guide, we’ll explain:

- what each Medicare part means

- what is covered under each plan

- the differences between Medicare Parts A, B, C, and D

- common Medicare costs

- how to choose the right coverage

By the end, you’ll have a much clearer understanding of how Medicare works and which parts may be important for your healthcare needs.

What Is Medicare?

Medicare is a federal health insurance program in the United States designed primarily for:

- people age 65 and older

- certain younger individuals with disabilities

- people with specific medical conditions

Medicare helps cover healthcare costs such as:

- hospital stays

- doctor visits

- medical treatments

- prescription drugs

Medicare is divided into different parts because each part covers a different type of healthcare service.

These include:

- Medicare Part A

- Medicare Part B

- Medicare Part C

- Medicare Part D

Let’s understand each one step by step.

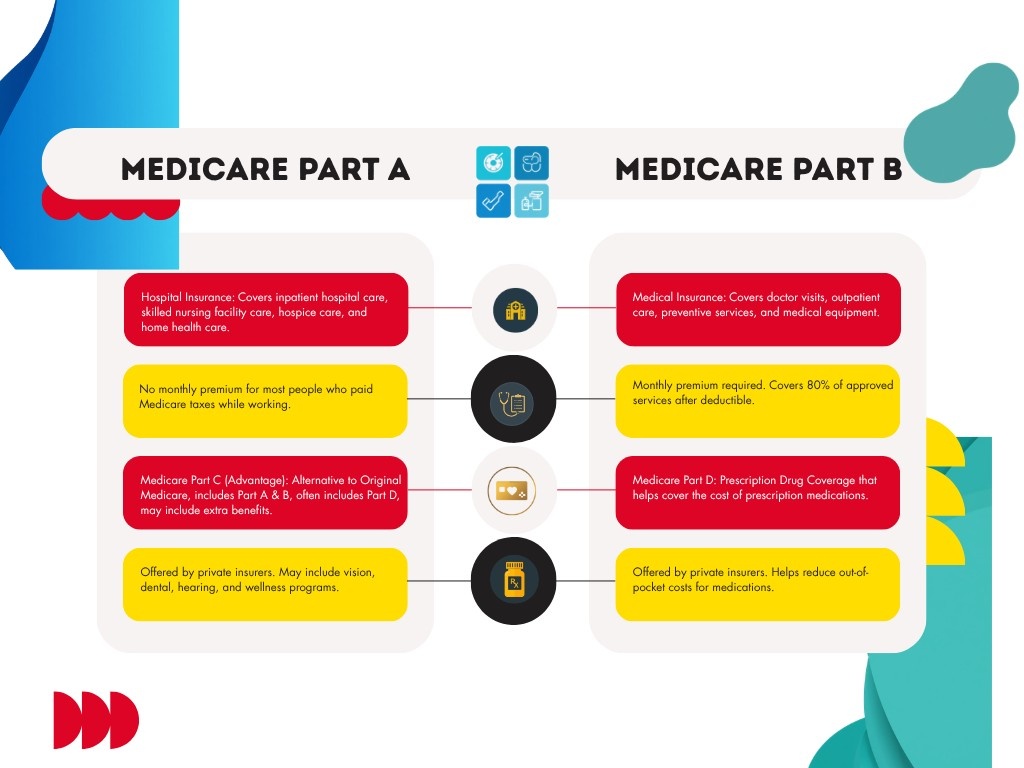

Medicare Part A Explained

What Is Medicare Part A?

Medicare Part A is commonly known as:

Hospital Insurance

It primarily helps cover costs related to:

- hospital stays

- inpatient care

- skilled nursing facilities

- hospice care

- some home healthcare services

What Does Medicare Part A Cover?

Part A generally covers:

| Covered Service | Examples |

|---|---|

| Inpatient Hospital Care | Hospital admission and overnight stays |

| Skilled Nursing Facility Care | Rehabilitation after hospitalization |

| Hospice Care | End-of-life support services |

| Limited Home Health Care | Certain medically necessary services |

What Medicare Part A Does NOT Cover

Part A usually does not cover:

- routine doctor visits

- outpatient care

- dental care

- vision exams

- hearing aids

- prescription medications outside hospital settings

Do You Pay for Medicare Part A?

Many people qualify for:

Premium-Free Part A

if they or their spouse paid Medicare taxes while working.

However, some individuals may still pay monthly premiums depending on work history.

You may also still pay:

- deductibles

- coinsurance

- copayments

for certain services.

Medicare Part B Explained

What Is Medicare Part B?

Medicare Part B is:

Medical Insurance

It helps cover outpatient and medically necessary healthcare services.

What Does Medicare Part B Cover?

Part B commonly covers:

| Covered Service | Examples |

|---|---|

| Doctor Visits | Primary care and specialists |

| Preventive Services | Screenings and vaccinations |

| Outpatient Care | Same-day procedures |

| Durable Medical Equipment | Wheelchairs, oxygen equipment |

| Mental Health Services | Therapy and counseling |

Preventive Benefits Under Part B

One important advantage of Part B is preventive healthcare coverage.

This may include:

- annual wellness visits

- diabetes screenings

- cancer screenings

- flu shots

- cardiovascular screenings

Preventive care can help detect health problems early.

Medicare Part B Costs

Unlike Part A, most people pay a:

monthly premium for Part B

Costs may vary depending on:

- income

- enrollment timing

- coverage choices

Part B also typically includes:

- annual deductibles

- coinsurance costs

Medicare Part C Explained

What Is Medicare Part C?

Medicare Part C is also known as:

Medicare Advantage

These plans are offered through private insurance companies approved by Medicare.

Part C combines:

- Medicare Part A

- Medicare Part B

and often includes:

- prescription drug coverage

- dental benefits

- vision coverage

- hearing benefits

- wellness programs

How Medicare Advantage Works

Instead of receiving healthcare directly through Original Medicare, your coverage is managed through a private insurance company.

Many Medicare Advantage plans function similarly to:

- HMOs

- PPOs

This means:

- provider networks may apply

- referrals may sometimes be required

- out-of-network care may cost more

Read our guide on PPO vs HMO.

Benefits of Medicare Part C

Additional Benefits

Many plans include services not covered by Original Medicare, such as:

- dental care

- vision exams

- hearing aids

- fitness memberships

Prescription Drug Coverage

Many Medicare Advantage plans include:

Part D prescription drug coverage

This creates an all-in-one healthcare plan.

Annual Out-of-Pocket Maximum

Most Medicare Advantage plans include annual spending limits, which can help protect against very large medical bills. Read our out-of-pocket maximum guide.

Disadvantages of Medicare Part C

Provider Network Restrictions

You may need to use:

- in-network doctors

- approved hospitals

for lower costs.

Prior Authorization Requirements

Some treatments or procedures may require approval before coverage is provided.

Coverage Rules Can Change Annually

Benefits, costs, and provider networks can change each year.

Medicare Part D Explained

What Is Medicare Part D?

Medicare Part D helps cover:

Prescription Drug Costs

These plans are offered by private insurance companies approved by Medicare.

What Does Medicare Part D Cover?

Part D may help cover:

- generic medications

- brand-name prescriptions

- specialty drugs

- vaccines

Each plan has its own:

- formulary (drug list)

- pricing structure

- pharmacy network

Why Medicare Part D Is Important

Prescription medications can become extremely expensive, especially for seniors managing chronic conditions.

Part D helps reduce:

- medication expenses

- out-of-pocket prescription costs

Medicare Part D Costs

Part D plans may include:

- monthly premiums

- deductibles

- copays

- coinsurance

Costs vary depending on:

- plan selection

- medications used

- pharmacy choice

Understanding Original Medicare

Original Medicare refers to:

Part A + Part B

This is the basic federal Medicare coverage.

However, Original Medicare does not cover everything.

This is why many people add:

- Medicare Supplement (Medigap)

OR - Medicare Advantage plans

to help reduce healthcare expenses.

Medicare Parts A, B, C, and D Comparison

| Medicare Part | Main Purpose | Coverage Type |

|---|---|---|

| Part A | Hospital Insurance | Inpatient care |

| Part B | Medical Insurance | Outpatient and doctor services |

| Part C | Medicare Advantage | Private bundled coverage |

| Part D | Prescription Drugs | Medication coverage |

Do You Need All Medicare Parts?

Not everyone needs every Medicare part.

Your ideal Medicare setup depends on:

- healthcare needs

- budget

- prescription medications

- doctor preferences

- travel habits

Common Medicare Coverage Combinations

Option 1: Original Medicare + Part D

This includes:

- Part A

- Part B

- Part D

Some people also add:

- Medigap coverage

Option 2: Medicare Advantage Plan

This usually combines:

- Part A

- Part B

- Part D

into one private plan.

Medicare Enrollment Periods Explained

Understanding enrollment timing is very important.

Missing deadlines may result in:

- penalties

- delayed coverage

- higher costs

Initial Enrollment Period (IEP)

This is your first opportunity to enroll in Medicare.

It usually begins:

- 3 months before turning 65

- includes your birth month

- continues for 3 months after

Annual Open Enrollment Period

This period usually runs:

October 15 to December 7

During this time, people may:

- switch Medicare Advantage plans

- change Part D plans

- return to Original Medicare

Medicare Advantage Open Enrollment

This period generally runs:

January 1 to March 31

People already enrolled in Medicare Advantage may:

- switch plans

- return to Original Medicare

Common Medicare Mistakes to Avoid

Delaying Enrollment

Late enrollment may result in:

- penalties

- gaps in coverage

Ignoring Prescription Drug Coverage

Even if you currently take few medications, future healthcare needs may change.

Choosing Plans Based Only on Premiums

Low premiums do not always mean lower overall healthcare costs.

Always consider:

- deductibles

- copays

- provider networks

- prescription costs

Not Reviewing Plans Annually

Healthcare needs and plan benefits change regularly.

Annual review is important.

Which Medicare Option Is Best?

There is no one-size-fits-all Medicare solution.

Some people prioritize:

- lower premiums

- extra benefits

- bundled convenience

Others prefer:

- provider flexibility

- predictable healthcare costs

- nationwide access

The best Medicare setup depends on your personal healthcare and financial situation.

Final Thoughts

Understanding Medicare Parts A, B, C, and D is the first step toward making informed healthcare decisions during retirement.

Here’s a simple recap:

- Part A covers hospital care

- Part B covers medical and outpatient services

- Part C combines Medicare benefits through private plans

- Part D helps cover prescription drug costs

While Medicare can initially seem confusing, learning the basics makes it much easier to compare plans and choose appropriate coverage.

Taking time to understand your options can help you avoid unexpected medical expenses and improve your long-term healthcare planning.

Frequently Asked Questions (FAQs)

What is the difference between Medicare Part A and Part B?

Part A mainly covers hospital care, while Part B covers outpatient medical services and doctor visits.

Is Medicare Part C the same as Medicare Advantage?

Yes. Medicare Part C refers to Medicare Advantage plans offered through private insurance companies.

Do all Medicare Advantage plans include prescription drugs?

Many do, but not all. Always review plan details carefully.

Is Medicare Part D mandatory?

It is not technically mandatory, but delaying enrollment without other creditable prescription coverage may result in penalties later.

Can you have Original Medicare and Medicare Advantage together?

No. You generally choose either:

Original Medicare or Medicare Advantage for your primary coverage.

Why You Should Compare Before Choosing

Health insurance pricing varies significantly between providers.

Two similar plans can differ by:

- $100–$300/month in premium

- Thousands in total yearly cost

👉 Comparing plans ensures you don’t overpay.

Compare Health Insurance Plans Based on Your Situation

The best way to find the right plan is to compare options based on:

- Your income

- Your state

- Your expected medical usage

Instead of guessing, use a comparison tool to see:

✔ Real monthly premiums

✔ Deductibles and out-of-pocket costs

✔ Subsidy eligibility

Explore More Health Insurance Guides

- How to Calculate Health Insurance Cost

- Bronze vs Silver vs Gold Comparison

- HDHP vs PPO Guide

- Open Enrollment Guide

👉 View all health insurance guides

About the Author

Shivakar Singh is the founder of Benefits Explained Simple, an educational platform focused on simplifying health insurance, workplace benefits, and financial decision-making. His work focuses on explaining complex benefit structures in clear, practical frameworks for working professionals.

“For a complete overview of how all these terms connect